Understanding How Mechanic’s Liens Impact Real Estate Transactions in Florida

Discover how mechanic’s liens protect contractors, subcontractors, suppliers, and workers in Florida’s fast-moving real estate market by securing payment for their work.

Last updated:

April 16th, 2026

Published:

August 13, 2025

3 mins

Read

Florida’s construction industry involves many moving parts—and one key but often overlooked piece is the mechanic’s lien. It helps protect contractors, subcontractors, suppliers, and workers who provide materials or labor to improve a property.

While essential for ensuring fair payment, mechanic’s liens can also complicate real estate transactions—delaying or even derailing sales, refinances, or major developments. That’s why it’s vital for property owners, buyers, lenders, and real estate professionals to understand how these liens work under Florida law and how they impact the flow of a real estate deal.

What Is a Mechanic’s Lien?

A mechanic's lien, also known as a construction lien, is a statutory claim against real property for services or materials supplied to improve the property. In Florida, the legal basis for these liens is primarily found in Chapter 713 of the Florida Statutes. This law grants individuals and entities who have contributed to the improvement of real property the right to place a lien on that property if they are not paid for their work or materials.

Those who can file a lien typically include:

- Contractors: General contractors directly contracted by the property owner.

- Subcontractors: Those who work for the general contractor.

- Suppliers: Entities that provide materials for the project.

- Laborers: Individuals who perform work on the property.

The primary purpose of a mechanic's lien is to secure payment for unpaid work or materials. It acts as an encumbrance on the property, providing a legal claim that can ultimately lead to foreclosure if the debt remains unpaid.

.jpg)

How Mechanic’s Liens Affect Property Titles

When a mechanic's lien is properly filed, it becomes a "cloud" on the property's title. This means that the ownership of the property is no longer clear and free of encumbrances. A clouded title can have significant repercussions:

- Impact on Title Insurance and Due Diligence: Title insurance companies are hesitant to issue clear policies on properties with outstanding liens, as the lien represents a potential claim against the property that the insurer would have to cover. During due diligence, a thorough title search will reveal any recorded liens, alerting potential buyers or lenders to the issue.

- Delay or Block Transactions: The presence of a lien almost always delays real estate transactions. Buyers are generally unwilling to purchase a property with an unresolved lien, as they could become responsible for the debt. Similarly, lenders will not approve a mortgage or refinance on a property with a clouded title, as their collateral would be compromised. This can effectively block a sale or refinance until the lien is addressed.

Mechanic’s Liens in Residential vs. Commercial Transactions

While mechanic’s liens apply to both residential and commercial properties, there can be differences in their impact and the considerations involved:

- Residential Transactions: In residential projects, homeowners often have specific protections under Florida law. For instance, the process for filing a lien on a homestead property can be more stringent. Owners in residential projects also have responsibilities, such as ensuring that their general contractor provides them with a "release of lien" or "final contractor's affidavit" upon final payment, indicating that all subcontractors and suppliers have been paid.

- Commercial Real Estate Deals: Commercial transactions often involve larger and more complex projects, leading to a higher volume of potential lienors (contractors, subcontractors, suppliers). The financial stakes are typically greater, and the parties involved are often more sophisticated in navigating lien laws. Special considerations include understanding the hierarchy of liens, the potential for multiple liens from various trades, and the broader financial implications for developers and investors.

Disclosure and Discovery of Liens

Transparency and due diligence are paramount when dealing with mechanic's liens:

- How Liens are Discovered: The most common way a lien is discovered is through a thorough title search conducted by a title company or attorney. This search examines public records for any encumbrances on the property's title, including recorded mechanic's liens.

- Seller's Duty to Disclose: While not explicitly always a legal requirement to verbally disclose every lien, sellers have a general duty to disclose known material defects that could affect the value or marketability of the property. An undisclosed lien, if known to the seller, could lead to legal issues. More importantly, the title search will inevitably reveal it, making it impossible to hide.

- Buyer's Options Upon Discovering a Lien: Upon discovering a lien, a buyer typically has several options:

- Demand Resolution: The buyer can demand that the seller resolve the lien before closing.

- Negotiate Price: If the buyer is willing to take on the lien, they might negotiate a reduced purchase price to cover the cost of resolving it.

- Terminate Contract: If the lien cannot be resolved or is too significant, the buyer may choose to terminate the purchase agreement.

.jpg)

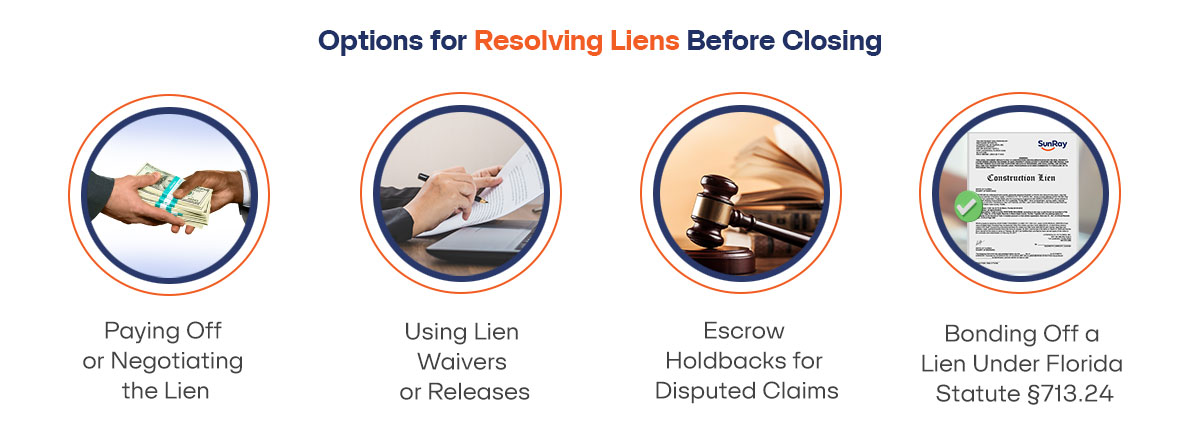

Options for Resolving Liens Before Closing

Addressing a mechanic’s lien proactively is crucial for a smooth transaction. Several options exist for resolution:

- Paying Off or Negotiating the Lien: The most straightforward solution is for the party responsible for the debt (usually the seller) to pay off the lienholder in full. Alternatively, negotiations can occur to settle the debt for a reduced amount.

- Using Lien Waivers or Releases: Lien waivers are legal documents signed by contractors, subcontractors, or suppliers, waiving their right to file a lien for work performed or materials supplied up to a certain date or for a specific payment. A "release of lien" is filed once the lien has been satisfied, removing the encumbrance from the title.

- Escrow Holdbacks for Disputed Claims: If a lien is disputed and cannot be resolved before closing, the parties may agree to an escrow holdback. A portion of the sale proceeds is held in an escrow account until the dispute is resolved, ensuring funds are available to pay the lien if necessary.

- Bonding Off a Lien Under Florida Statute §713.24: Florida law allows for a lien to be "bonded off." This involves depositing a cash bond or surety bond with the clerk of the court in an amount equal to the amount of the lien plus interest and potential attorney's fees (typically 125% of the lien amount). This effectively transfers the lien from the property to the bond, allowing the real estate transaction to proceed while the dispute over the lien is litigated.

Preventing Mechanic’s Liens in Future Transactions

Prevention is always better than a cure when it comes to mechanic’s liens:

Best Practices:

- Notices to Owner (NTOs): In Florida, most lienors (except general contractors) are required to serve a Notice to Owner (NTO) within 45 days of beginning work or delivering materials. Property owners should be diligent about tracking these NTOs.

- Lien Waivers: Always obtain progressive and final lien waivers from contractors, subcontractors, and suppliers as payments are made.

- Final Affidavits: Before making the final payment to a general contractor, obtain a final contractor's affidavit stating that all lienors have been paid or listing those who have not.

- Role of Contractors and Property Owners: Contractors should be meticulous in their billing and payment practices. Property owners should exercise due diligence, verify licenses, and ensure proper contracts are in place. Open communication can prevent many disputes.

- The Importance of Working with Lien-Savvy Professionals: Engaging experienced title agents, real estate attorneys, and construction lawyers who understand Florida's lien laws is invaluable. They can guide parties through the complexities, review documents, and advise on best practices to avoid and resolve lien issues.

Legal Risks for Buyers and Sellers

Mechanic's liens pose distinct legal risks for both parties in a real estate transaction:

- Risks for Buyers: Inheriting Unresolved Liens: The primary risk for a buyer is unknowingly acquiring a property with outstanding lien. If the lien is not resolved before closing, the buyer could become responsible for paying the debt to clear the title, even though they didn't incur the original debt. This can lead to significant financial burdens and legal battles.

- Risks for Sellers: Breach of Contract, Delayed Closing: For sellers, an unresolved lien can constitute a breach of the sales contract, which typically stipulates that the seller will deliver clear title. This can lead to the buyer backing out, the loss of a deposit, or even a lawsuit for specific performance or damages. More commonly, it results in delayed closing, which can have financial penalties and logistical headaches.

- Remedies and Legal Recourse: Both buyers and sellers have legal remedies. A buyer might sue a seller for fraudulent misrepresentation or breach of contract if a lien was concealed. A seller might sue the lienor for slander of title if the lien was improperly filed. The lienor itself has the right to foreclose on the lien if not paid.

Mechanic’s Liens and Lender Concerns

Lenders play a critical role in real estate transactions, and mechanic's liens are a major concern for them:

- How Liens Complicate Mortgage Approvals: Lenders require their loans to be secured by a first-priority lien on the property. A mechanic's lien, especially if filed before the mortgage, can take precedence, jeopardizing the lender's security interest. This makes lenders extremely wary of approving mortgages on properties with existing liens.

- Lender Requirements Before Disbursing Funds: Before disbursing loan funds, lenders will typically require a clear title. This means any existing mechanic's liens must be satisfied, released, or bonded off. They will often rely on the title insurance company's commitment to ensure their interest is protected.

- Special Considerations for Construction Loans: In construction loan scenarios, lenders are particularly vigilant. They often implement strict disbursement schedules, requiring lien waivers at each draw to ensure that funds are being used to pay contractors and suppliers, thereby mitigating the risk of future liens. They may also require performance and payment bonds from the general contractor.

Key Takeaway

Mechanic's liens are a powerful and complex aspect of Florida real estate law. Their ability to encumber property titles means they can significantly impact real estate transactions, leading to delays, disputes, and financial losses if not properly managed. For all parties involved – buyers, sellers, and lenders – understanding the mechanics of these liens, their potential impact, and the available resolution and prevention strategies is not just beneficial, but absolutely crucial. Proactive due diligence, clear communication, and the indispensable guidance of experienced legal and title professionals are the best defenses against the challenges posed by mechanic's liens, ensuring smoother and more secure real estate dealings in the Sunshine State.

To better understand your lien rights, check out our guides on the Notice to Owner Florida and the Florida Mechanics Lien.

Protect Your Rights with a Notice to Owner

Sending a notice to owner is the first step to secure payment on construction projects. Learn how a notice to owner Florida helps protect your lien rights and ensures you get paid.

Protect Your Payment Rights with Florida’s Most Trusted Notice & Lien Services

Notice to Owner – Secure your lien rights early. File your NTO now!

Notice to Owner Florida – Stay compliant with Florida deadlines. Send your NTO today!

Mechanics Lien Florida – Get paid faster. Start your Florida lien process now!

Notice to Owner Florida – Don’t Risk Your Lien Rights

Stay compliant with Notice to Owner Florida requirements. Send your Notice to Owner today and protect your payment.

Florida Construction Forms – Protect Your Lien Rights

Stay protected on your construction project. Send your Notice to Owner Florida and preserve your lien rights with a timely Notice to Owner .

Notice of Commencement Florida Form – Record a Notice of Commencement to officially start the project and establish key lien deadlines.

Florida Mechanics Lien Form – File a Mechanics Lien to secure payment when contractors or suppliers are unpaid.

Contractor’s Final Payment Affidavit Florida Form – Submit a Contractor’s Final Payment Affidavit before final payment to comply with Florida lien law.

Notice of Nonpayment Florida Form – Send a Notice of Nonpayment on bonded projects to preserve your right to a bond claim.

Notice of Termination Florida Form – Use a Notice of Termination to properly end a Notice of Commencement and reset lien timelines.

Miller Act Claim Form – File a Miller Act Claim to recover payment on federal construction projects.

Free Florida Lien Waiver and Release Form – Download a Florida Lien Waiver and Release to exchange payment for lien rights safely.

Start your Notice to Owner or file a Notice to Owner Florida today to protect your lien rights. If payment issues arise, secure your claim with a Mechanics Lien Florida filed quickly and correctly.

Frequently Asked Questions (FAQs)

What is a mechanic’s lien in Florida real estate?

A mechanic's lien, or construction lien, is a legal claim against real property in Florida by contractors, subcontractors, suppliers, or laborers who have not been paid for their work or materials used to improve that property. It serves as an encumbrance on the property's title.

Can a property be sold with a mechanic’s lien on it?

While technically possible, it is highly impractical and risky. Most buyers and lenders will not proceed with a sale or finance a property that has an unresolved mechanic's lien, as it clouds the title and creates potential financial liability for the new owner.

How can a buyer find out if a property has a lien?

A buyer can discover if a property has a lien through a professional title search, which is typically conducted by a title company or real estate attorney as part of the due diligence process.

What steps can a seller take to remove a lien before closing?

A seller can remove a lien by:

- Paying off the lien in full or negotiating a settlement with the lienholder.

- Obtaining a formal release of lien from the lienholder once paid.

- Bonding off the lien by depositing a cash or surety bond with the court, which transfers the lien claim from the property to the bond.

How do mechanic’s liens affect title insurance?

Mechanic's liens create a risk for title insurance companies. They will typically refuse to issue a "clean" title insurance policy on a property with an outstanding lien until the lien is resolved, as they would be obligated to cover the costs associated with the lien if it were to result in a claim.

Is a lien valid if the contractor didn’t finish the job?

The validity of a lien when a contractor didn't finish the job can be complex and depends on the specific circumstances and contract terms. The lien amount would typically be limited to the value of the work actually performed or materials supplied. Such situations often lead to legal disputes over the quality or completion of work.

Can liens be bonded off in Florida?

Yes, under Florida Statute §713.24, a property owner can "bond off" a mechanic's lien. This involves depositing a bond (cash or surety) with the clerk of the court, typically 125% of the lien amount, which transfers the lien from the property to the bond. This allows the property to be sold or refinanced while the dispute over the lien's validity or amount is resolved separately.

How long does a mechanic’s lien stay on a property in Florida?

In Florida, a mechanic's lien generally expires one year from the date it was recorded unless a lawsuit to enforce the lien is filed within that timeframe. If a lawsuit is filed, the lien remains active until the legal proceedings are concluded.

What happens if a lien is discovered after closing?

If a valid lien is discovered after closing, the new property owner may be responsible for paying it, depending on the circumstances and the terms of the sale. This is why a thorough title search and title insurance are crucial, as title insurance may provide coverage for such undisclosed liens. To help prevent such issues, it’s important that proper notices such as a notice to owner or notice to owner Florida are correctly served during the project lifecycle.

Who is responsible for paying off a lien—buyer or seller?

Typically, the seller is responsible for paying off any outstanding mechanic's liens before or at closing, as part of their obligation to deliver clear title to the buyer. However, in some negotiated scenarios, a buyer might agree to assume the lien in exchange for a price reduction, but this is less common and carries significant risk for the buyer.

FAQs: Fundamentals of Lien Laws

Ariela C. Wagner

.jpg)

.jpg)

.jpg)

.jpg)